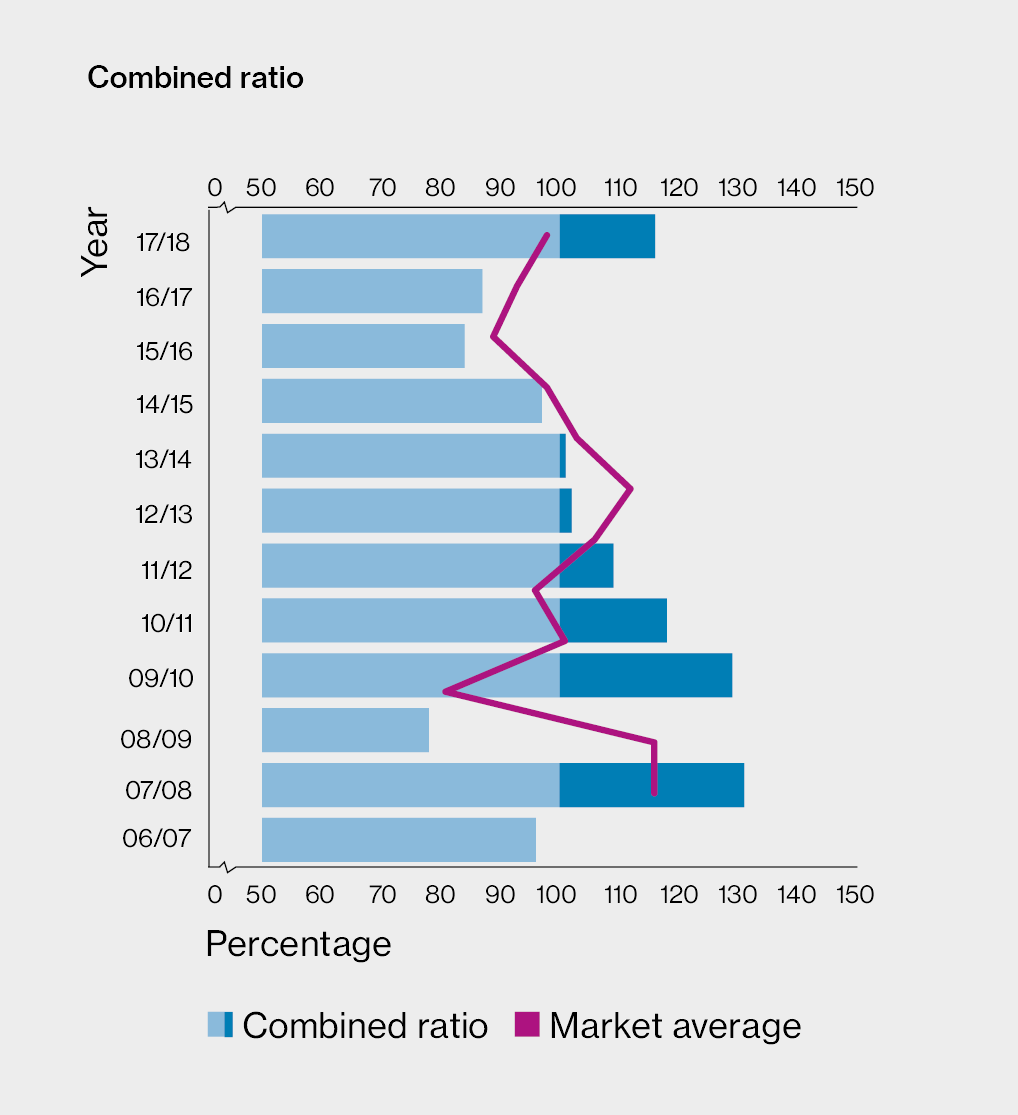

The West of England’s net combined ratio deteriorated from 87% to 116% between 2016/17 and 2017/18. This is the first underwriting defecit reported by the Club since 2013/14.

| 2015/16 | 2016/17 | 2017/18 | |

|---|---|---|---|

| Income and Expenditure | |||

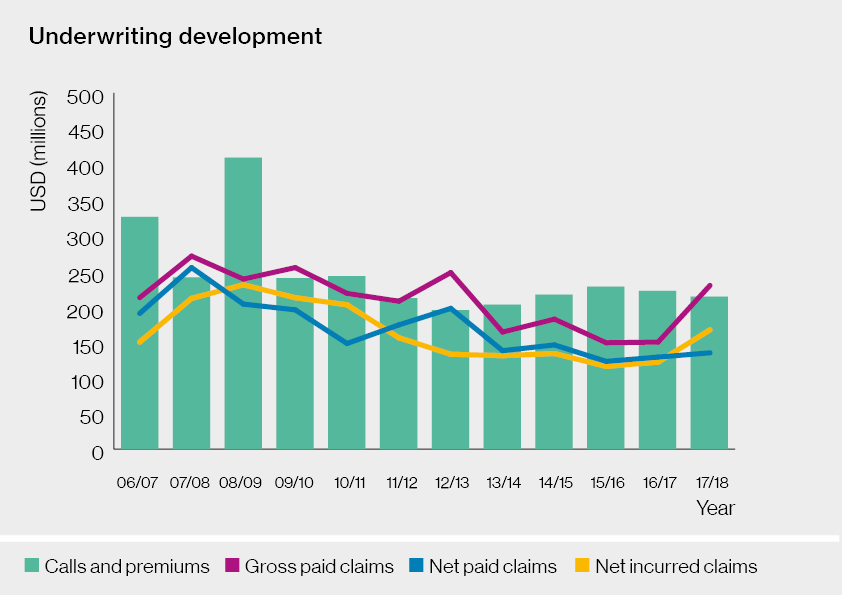

| Calls and Premiums | 227,614 | 221,849 | 213,797 |

| Reinsurance Premiums | -43,927 | -40,172 | -37,4962 |

| Operating Expenses | -35,466 | -34,688 | -35,392 |

| Operating Income | 148,221 | 146,989 | 140,909 |

| Gross Paid Claims | 150,528 | 151,540 | 230,979 |

| Net Paid Claims | 124,853 | 130,788 | 136,844 |

| Net Change in Provision for Claims | -6,781 | -7,016 | 32,299 |

| Net Incurred Claims | 118,072 | 123,772 | 149,143 |

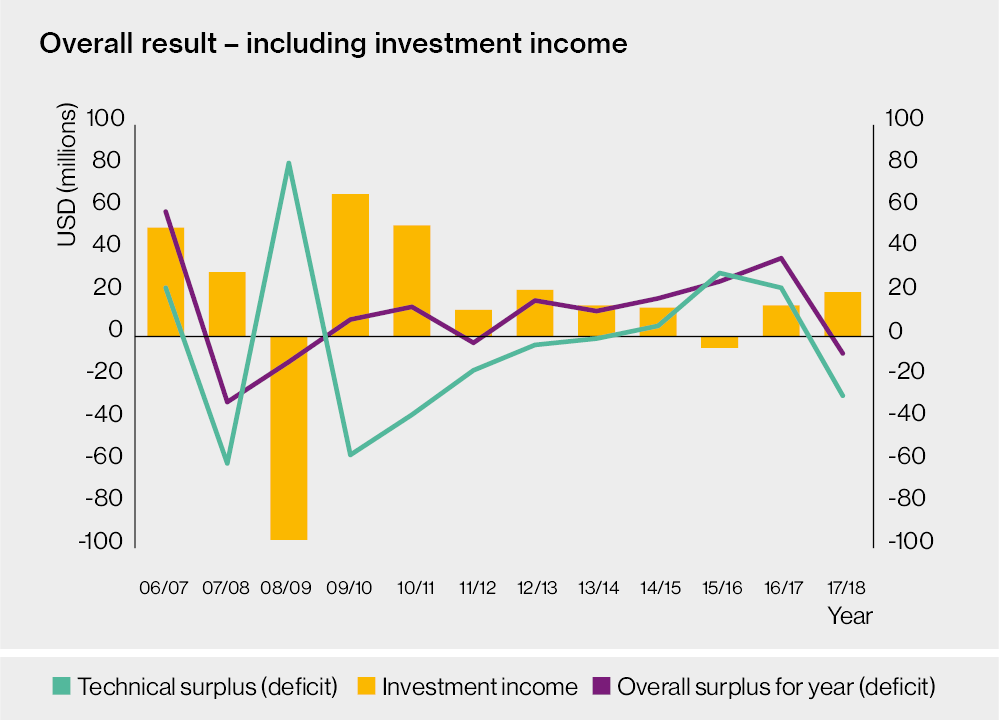

| Technical Surplus (Deficit) | 30,149 | 23,217 | -28,234 |

| Investment Income | -4,527 | 13,758 | 20,017 |

| Overall Surplus for Year (Deficit) | 25,622 | 36,975 | -8,217 |

| Balance sheet | |||

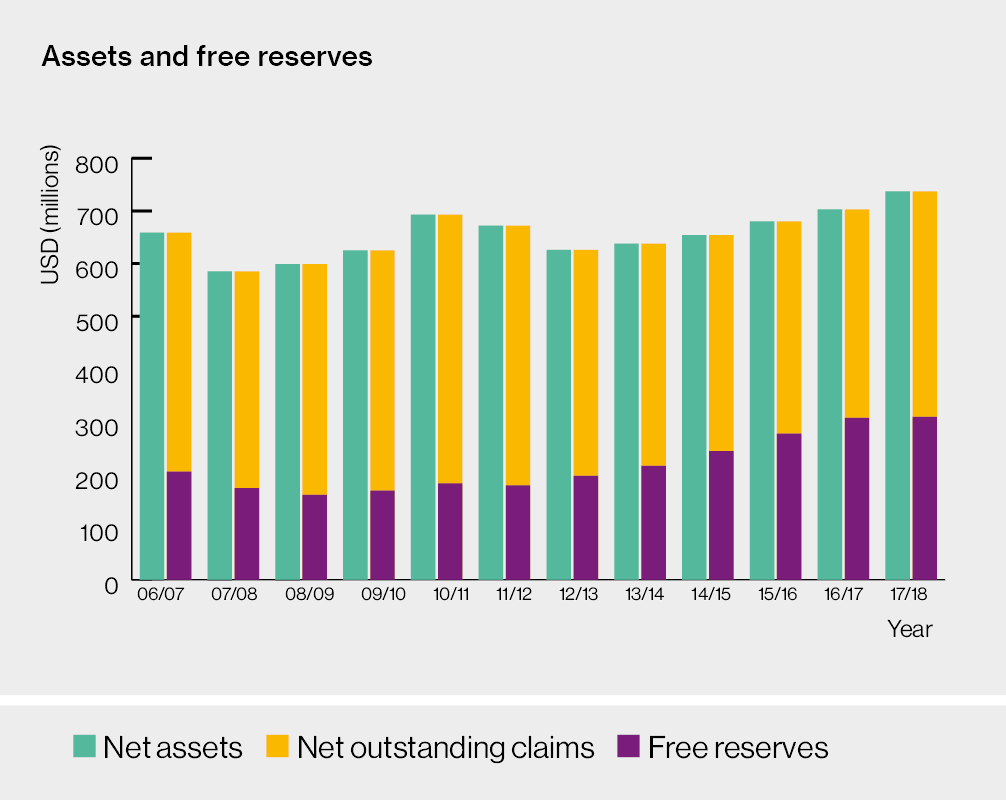

| Net Assets | 680,166 | 703,001 | 737,321 |

| Net Outstanding Claims | 403,505 | 396,489 | 428,788 |

| Free Reserves | 276,661 | 306,512 | 308,533 |

| Entered tonnage (GT, millions) | 2016 | 2017 | 2018 |

|---|---|---|---|

| Owned / Mutual | 72.1 | 82.5 | 90.6 |

| Chartered / Fixed | 28 | 30 | 29.4 |

| Total | 100.1 | 112.5 | 120.0 |

| S&P Rating History | 2016 | 2017 | 2018 |

| BBB+ | A- | A- | |

| Average Expense Ratio (AER) | 2016 | 2017 | 2018 |

| Five years ending 20 February | 15.5 | 15.2 | 14.8 |

Combined ratios provide a direct comparison of club underwriting performance. The combined ratio is essentially the net loss ratio for the club and is defined as follows:

Combined ratio = |

(Net incurred claims + operating expenses) |

|---|

Average Expense Ratios (AERs) were introduced in 1999 following pressure from the European Commission in an attempt to enable direct comparisons of operating costs between clubs within the International Group. The formula that all clubs are required to adhere to when calculating their AER figure is as follows:

The AER formula is the |

(Operating expenses x 100) |

|---|

In principle the AER is a reasonable idea, but in reality it is only ever a very approximate guide to the relative operating costs of individual clubs. For example different membership profiles, disproportionately high levels of premium or investment, whether the club owns or rents their office space, how much the club spends on loss prevention, global office network, member portals etc all have an impact on the AER.